In this post, I’m going to explore the pricing dynamics within the bike industry from COVID until present day and summon my crystal ball to see what we might expect into the future. As always, anytime I’m making a prediction, it should be taken with a giant grain of salt, reader beware.

The forces shaping bike industry pricing today include tariffs, foreign exchange turbulence, supply chain complexity, the limits of scaling laws on technology, lingering COVID effects, economies of scale, interest rates, and the number of players in the market. If that list makes your head spin, don’t worry, we’ll break it down step by step to understand how we got here and what it might signal about the future. To add perspective, I’ll also draw on Michael Mauboussin’s classic framework, Measuring the Moat, to see what it suggests about where the industry could be headed.

Thanks for reading Jeff’s Newsletter! Subscribe for free to receive new posts and support my work.

The Pandemic

To the uninitiated, much of today’s pricing dynamics still trace back to the pandemic. I’ve written at length about this elsewhere (links at the bottom of this post), but the short version is simple: COVID created a massive oversupply at the same time consumer demand weakened. Even in 2025, you can still find COVID-era bikes or components sitting on dealer floors or in warehouses around the world. And for anyone who remembers Macro 101, when supply far exceeds demand, prices fall.

Between 2023 and 2025, the industry was flooded with heavy discounts, and plagued by bankruptcies and restructurings. As one example, I picked up a brand-new current model year Specialized Stumpjumper with a $6,000 MSRP for around $3,500 in the middle of the summer. Great deal for me as a consumer, but disastrous for the companies making and selling these bikes. Cash flows slowed, margins collapsed, and the future looked uncertain.

The Consumer

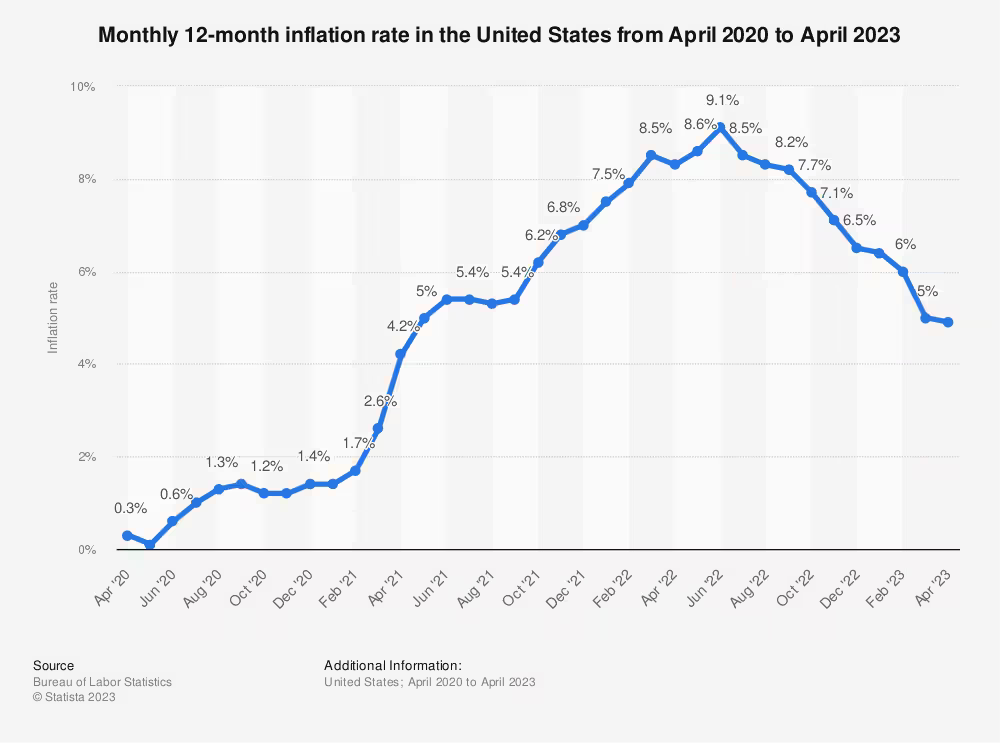

The pandemic and its aftermath reshaped consumers across the entire economy, but the bike buyer has some unique characteristics worth unpacking. Two of the biggest forces driving behavior in this market have been rapid inflation and the sharp rise in interest rates.

The pandemic’s end was followed by a surge of inflation not seen since the 1970s. No industry was spared, and prices across the economy climbed sharply. While some sectors experienced wage growth that helped offset the shock, many did not. The result was a broad swath of consumers who simply felt poorer in the face of higher prices. Bike related purchases aside a good chunk of consumers felt more poor with less discretionary income than they had prior to this period of inflation.

Rising interest rates don’t affect bike buyers as directly as they do powersports consumers, where financing is a core part of the purchase. But higher rates still matter. When mortgages, car loans, and other obligations become more expensive, discretionary income shrinks and spending on bikes takes a hit. Beyond that, rising rates tend to cool the broader economy, eroding consumer confidence and leaving people feeling less wealthy overall.

As a data point, credit card balances have ballooned roughly 39% since 2021. While this is more of a marker than a direct catalyst, it’s an important signal. Rising balances suggest two things. First, consumers have less cash on hand than they did previously. Second, many are leaning on credit at higher rates, effectively sliding into a mild debt spiral.

A quick aside: wealth cushions these effects. If you own meaningful assets, inflation often works in your favor your holdings rise in value as currency erodes. Rising rates may compress equity multiples, but let’s be real the S&P just hit an all-time high. If you’re in that bracket, you’re probably doing fine and can buy whatever bike you want. The real issue is that most Americans don’t fall into that camp.

The big point to takeaway from this section is this: a large share of bike buyers simply aren’t spending the way they once did. That’s what we mean by “consumer softness.”

Bike Technology

Technology has long been a key driver of inventory turns and pricing in the mountain bike industry. But the pace of real innovation slowed sharply right around the time COVID-19 shut the world down. Drawing on my tech background, I’d argue that scaling laws have always applied here: for the past 25 years, the industry has seen rapid gains year over year, but now we’ve hit the flat tail of the curve. Innovation today is incremental, not transformative. The actual performance differences are small; far smaller than the marketing hype would have us believe.

Bikes released in 2020 or 2021, like the Specialized Enduro or Transition Spire, still hold up today and are regularly seen atop podiums around the world. By contrast, more recent releases, such as the Stumpjumper 15, aren’t meaningfully faster in controlled testing than the prior generation. Speaking as a product tester, the year-over-year gains now feel smaller than at any point I’ve experienced.

There are upsides to this slowdown: manufacturers can amortize tooling costs over longer time horizons, which should, in theory, help stabilize or lower prices. But the downside is clear, riders have less incentive to upgrade with each new release*. Inventory turns will slow as more consumers wait until their current bike or components wear out rather than rushing to buy the latest model.

This isn’t unique to bikes. Most industries eventually reach a maturity curve where innovation shifts from hyper-progression to incremental refinement. Skis, for example, evolved dramatically between 2000 and 2012 in width, camber, and sidecut profiles, but innovation since then has been marginal. The industry didn’t die, but the economic and pricing dynamics changed, and the bike industry is now heading into that same phase.

(*exception to this statement; high end products in specific niches will likely continue to see rapid upgrade cycles, such as suspension products in addition to e-bikes, which I believe are still seeing notable improvements year over year)

Economic Policy Impact

The bike industry depends on a highly global supply chain, so it’s no surprise that tariffs from the Trump administration have had an outsized impact. While this topic could easily warrant its own deep dive, the bottom line is straightforward: tariffs are driving up costs and injecting uncertainty into the system.

Broadly speaking, I expect landed costs on most Asian-made products to rise 10–25%, with European goods climbing 5–15%. These figures are fluid, of course, given the volatility of current trade policy. Some of these increases are already visible on showroom floors, and I expect that trend to continue into 2026.

Currency weakness is another factor. The US dollar is down roughly 10% against the Euro and about 7% against the New Taiwan dollar, thanks to policy uncertainty, inflationary pressures, and a repricing of “US exceptionalism.” This effectively acts as another tax on American consumers—our dollars don’t stretch as far abroad. The flip side is that weaker dollars make US-made products more attractive to overseas buyers, which could benefit domestic brands in markets like Europe.

As for reshoring, I don’t expect meaningful bike manufacturing to return to the US anytime soon. Companies like Fox may move some assembly stateside, but large-scale manufacturing is unlikely. The barriers aren’t about labor or wages—it’s about capital requirements and the technological edge Asia maintains. Tariffs alone aren’t enough to change that equation, and it’s hard to see it shifting materially before the end of this administration.

Big picture: expect new bikes hitting showroom floors in late 2025 and into 2026 to be 5–35% more expensive than they would have been without these policies.

2026 Expectations

As we look toward 2026, the outlook is clear: consumers feel less wealthy, products will be more expensive, and the deep discounts we grew used to are fading. It’s a triple whammy. The $3,500 “steal” I scored on a high-end bike in 2023 is unlikely to repeat—by 2026, a comparable ride will probably run $6,000–$7,000.

Faced with that sticker shock, and with technological progress slowing, I may just patch up my current bike and keep riding it another season. And I expect many other riders will make the same choice.

If I’m a shop owner, I’m going to keep this in mind with my ordering for the upcoming season. If I’m a manufacturer, I’m probably going to do whatever I can to tighten my SKU count and offer the absolute best deals to my shops/consumers to incentivize a sale. We are all going to have to get creative if we want to see healthy inventory turns and strong sell through metrics.

2027 and Beyond

If 2026 shapes up as a difficult year, rising prices colliding with a softer consumer, the years beyond could look different. Over time, we may see tailwinds emerge: falling prices, a shrinking gap between “entry-level” and “top-tier” bikes, and longer tooling cycles that let brands spread costs over more years. This trend is already underway and shows no sign of reversing.

Here, I lean on Michael Mauboussin’s classic paper Measuring the Moat. His argument is clear: as industries mature, competitive moats erode, and product differentiation narrows, pricing power falls. The bike industry is no exception.

The evidence is everywhere. By 2025, bike designs have converged. In 2010, only a handful of bikes were truly compelling; today, the market is flooded with great options, with a high number that not only perform the same, they even look the same. Innovations that move the needle, say as a more recent example, devices to manage pedal kickback, are quickly copied across the industry, patents or not. Differentiation fades fast.

In this environment, price becomes the main battleground. To borrow Jeff Bezos’s line, “your margin is my opportunity.” The companies that thrive will be those large enough to exploit scale: efficient manufacturing, lower capital costs, tighter supply chains. After all, your bottom rung net margin you can survive at is driven by your weighed average cost of capital, and its no secret larger companies generally win on this front.

Consumers will benefit from high-performing bikes at reasonable prices, while the “swanky” top-end offerings deliver only marginal gains over stock builds, similar to what we already see in powersports.

But there’s a dark side. The middle of the barbell will continue to hollow out. Smaller and mid-scale companies won’t be able to compete on price, and consolidation or roll-ups are the likely outcome. Bespoke brands like Moots and Unno will survive, but they’re competing on craftsmanship, high amounts of brand equity, and exclusivity, not scale.

Policy could also play a role. If a new administration rolls back tariffs, that would accelerate the downward pressure on prices. But regardless of politics, the structural trajectory is clear: the bike industry is entering its mature phase, where competition is won by size, efficiency, and the relentless grind of price.

Final Thoughts

Whew. There’s a lot going on in the industry these days. If there’s one overarching thought, it’s that I wish we could get back to an era where operators focused on running their companies and shops—not on what the Fed might do, whether Trump wakes up on the wrong side of the bed, or how to hedge against currency swings. These distractions spread everyone too thin, and we’re worse off for it.

I don’t have a crystal ball, and yes, some of this outlook—especially for 2026—sounds a bit doom and gloom. But there are bright spots. NICA has never been stronger, the sport is still as fun as ever, and it’s not going away. For business owners, doubling down on your core strengths and value proposition will pay dividends. For consumers, we may be entering an era where it makes more sense to maintain and enjoy the bike you already own, which isn’t a bad outcome. And longer term, falling prices and a narrowing performance gap between entry-level and top-tier bikes may actually make the sport more accessible.

At the end of the day, it’s still a great time to be a bike rider—despite all the chaos in the world. And I like that. Cheers everyone. As always, feel free to contact me at jeff.brines@gmail.com—whether it’s to talk bikes, software, or CFO’ing, I’m always down to chat.

Links: